Vancouver, B.C. – Martin Vydra, President of Giga Metals Corp. (TSX.V-GIGA), today provided a summary of an internal analysis that compares Giga’s Turnagain project to High Pressure, High Temperature Acid Leach (HPAL) projects both producing and in development.

“Our Preliminary Economic Assessment (PEA), announced October 28, 2020, modelled a mine that would produce an average of 33,000 tonnes per year of nickel over a mine life of 37 years with marginal economics at current nickel prices,” said Mr. Vydra. “The nickel would be contained in an exceptionally clean sulphide concentrate grading 18% nickel and 1% cobalt, suitable for smelting and refining into Class I nickel, as modelled in the PEA. We are also planning to conduct further testwork to confirm the amenability of Turnagain concentrate to direct refining via hydrometallurgy into recovered nickel suitable for the battery industry whether it be powder, briquettes or sulphate. We note that Sherritt International’s Fort Saskatchewan refinery, Voisey’s Bay Long Harbor refinery and BHP’s Kwinana refinery were all designed to directly refine nickel concentrates of similar composition.”

Mr. Vydra added, “One of the key benefits of Turnagain is the ability of the waste residue to absorb CO2 from the atmosphere. This is supported by Dr. Greg Dipple’s work at UBC and Giga Metals will be advancing work in 2021 in an effort to quantify the sequestration in order that data can be applied to future technical reports. In speaking to OEM’s, battery manufacturers and institutional investors, the potential for Turnagain to be a carbon neutral nickel mine without the need to purchase offset credits has significant value. This value is not reflected in the basic economic analysis conducted in the PEA. Aside from the potential to be able to generate revenue from selling excess CO2 credits, investors and consumers wishing to secure carbon neutral and ethical nickel have indicated that they would ascribe a premium to a nickel mine that was genuinely carbon neutral.”

A market study by Wood Mackenzie estimates that demand for nickel from battery manufacturers will rise from a current 170,000 tonnes per year (2019) to 700,000 tonnes per year by 2030 and to 1,600,000 tonnes per year by 2040, driven largely by demand for electric vehicles (EV). To satisfy that demand, allowing for some displacement of Class I nickel from current uses, up to fifteen new mines in the range of 35,000 tonnes of nickel per year would have to come onstream by 2030, plus a further 25 mines of a similar size by 2040.

“The market believes that most of the demand for battery grade nickel will be filled by new HPAL projects which are expected to be built within schedules and budgets that are unprecedented compared to the previous HPAL operations that have been commissioned in the last 25 years” said Mr. Vydra. “These projects, like the Turnagain project, have marginal economics at current nickel prices. Wood Mackenzie estimates that the average HPAL project in development would require a nickel price of US$10.86 per pound to provide a pre-tax Internal Rate of Return (IRR) of 12%. We wanted to understand how our project stands relative to HPAL projects in terms of pure economics, capital and technical risk, and environmental impact.”

ECONOMICS AND CAPITAL RISK

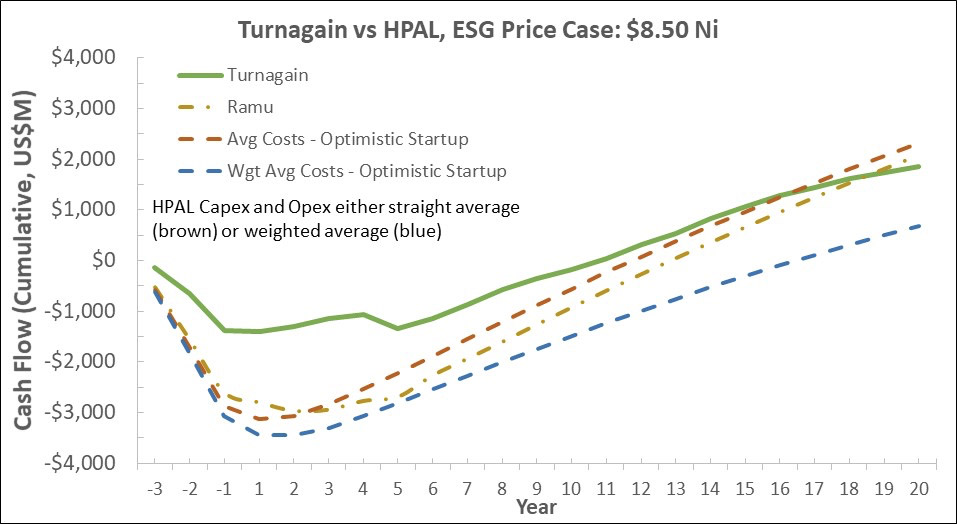

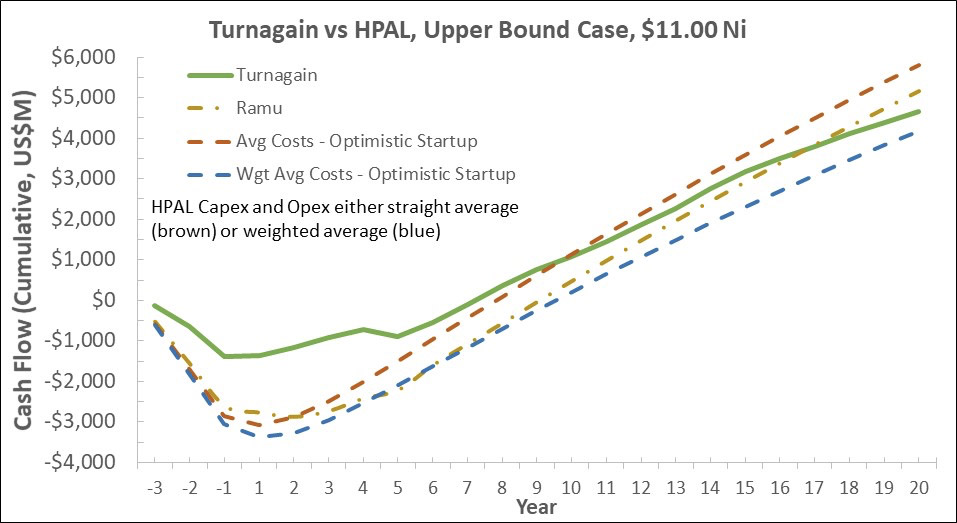

“We decided to compare ourselves to an operating HPAL project and to a basket of projects under study,” said Lyle Trytten, Giga Manager of Development. “Ramu, located in Papua New Guinea, is among the most successful HPAL projects built in the last 25 years. It was commissioned in 2012, but we updated their Capex to 2020 dollars for the analysis. The development projects in our analysis are of a range of capacities and located in Australia and the Philippines.”

Mr. Trytten continued “Our recently completed PEA included a sensitivity analysis around nickel price. While Wood Mackenzie provided long term nickel price guidance of US$7.50/lb (Base Case) and US$8.50/lb (ESG Case), they commented that the incentive price for new Western World HPAL projects is higher at $10.86/lb. We developed cumulative cash flow comparisons using the PEA model at the ESG Case and the lower and upper bounds of the sensitivity analysis, US$6.00/lb and US$11.00/lb, to understand our competitive positioning. In all cases, cobalt pricing is US$22.30/lb.”

“In all pricing scenarios, Turnagain is competitive with these types of projects and represents a lower capital risk,” said Mr. Trytten. “The project works well if built in two stages, so less money is on the line to achieve similar nickel production rates as the more capital intensive HPAL projects. Of course, we could always build Turnagain in a single exercise, improving financial returns.”

As noted in the PEA, the price sensitivity analysis range runs from a pre-tax IRR of 0.2% to 15.7%, and from a pre-tax NPV of -US$1,035 million to US$1,519 million. “At all the sensitivity pricing cases examined, Turnagain’s IRR and NPV are comparable if not superior to HPAL projects we understand are being contemplated,” said Mr. Trytten. While there is no prediction that any of these prices will occur, they offer comparison points for Turnagain against new HPAL projects.

TECHNICAL RISK

The Turnagain project is designed as an open pit mine with a very simple processing circuit. Mined material is crushed, ground, and put through froth flotation comprising a rougher circuit and three stages of cleaning to produce a sulphide concentrate for shipping. The technology has been used reliably for many decades in sulphide nickel, copper, and zinc mines, and there is nothing experimental or complex in the processing circuit. Ramp up times to full capacity for this type of simple circuit are from 6 to 18 months. Technical risk is considered very low.

HPAL projects strip mine nickel in fine-grained limonite ores, often with significant clay content, which are pumped into high-pressure autoclaves for treatment with large amounts of sulphuric acid at high temperatures. These complex facilities must deal with corrosive solutions, large-scale dissolution and re-precipitation of solids, sealing of the rotating shafts of pumps and agitators at the extreme conditions, and significant erosive steam flashing for heat recycle, resulting in exotic and expensive materials of construction and significant maintenance challenges. Ramp up times to full capacity are from 3 to 6 years, and some projects never reach name plate capacity. Technical risk is considered very high and every new process innovation adds risk.

ENVIRONMENTAL IMPACT

Turnagain is located in an area of very low seismic risk and relatively low precipitation. Designed as an open pit mine, the area of disturbance is moderate relative to the volume of material processed. The tailings management facility is designed to the highest safety standards. The mine residue will be mostly basic minerals with a very low percentage of unrecovered sulphides, so risk of acid generation is exceptionally low.

Power will be sourced from the provincial grid which is principally supplied with hydroelectric power, and the mine residue is known to sequester CO2 from the atmosphere, something Giga is actively researching. Our goal is to be the world’s first carbon neutral mine. Another advantage is that, as the silicate sand residue absorbs CO2 and converts to carbonate minerals, it undergoes a process of cementation that will further increase the stability of the tailings management facility.

HPAL projects under development outside of Australia are mostly contained within the “coral triangle”, an area of the Pacific Ocean that is recognized as the global center of marine biodiversity and a global priority for conservation, and it is an area of high seismic risk and very high precipitation.

The clay deposits are relatively thin and support rare tropical rainforests, which are cut down as the deposits are strip mined over a wide area relative to the volume of material processed. (The rainforests are rare because they are adapted to high nickel content in the soils). The fine-grained deposits are prone to significant erosion into streams, rivers, and the ocean.

Once mined and processed, dealing with mine waste, which is in the form of a slurry with extremely fine particle size, is a very difficult problem. The fine particles can be separated from solution and stored in a tailings management facility, but high rainfall and high seismic activity in the coral triangle area of the Pacific add risk and complexity to tailings storage. Many HPAL projects that are planned for these areas will require ocean disposal of their effluent regardless of their tailings management plans.

HPAL projects require large amounts of heat as well as power that is generally supplied by burning coal or other fossil fuels. They also use limestone to neutralize excess acid, which causes significant CO2 emissions from the limestone. They are very large CO2 emitters, with emissions in the range of 25 tonnes of CO2 emitted per tonne of nickel produced, and higher during their frequently prolonged ramp-ups.

“Based on Western environmental standards and Return on Investment required by Western producers, it is difficult to understand why HPAL projects are being considered by Western organizations,” said Mr. Vydra. “However, the strategic consideration of securing long term supplies of battery grade nickel combined with an extremely low cost of capital is incenting the Chinese, among others, to build these projects. Securing decades worth of nickel supply at the cost of production will provide a long term competitive advantage to battery and electric vehicle manufacturers.”

Technical information in this press release has been approved by Lyle Trytten, P.Eng., a Qualified Person as defined by NI 43-101. Financial modelling used herein is based on the Preliminary Economic Assessment (PEA) results released on October 28, 2020 that were authored by Hatch Ltd, a global engineering firm. The PEA includes the use of inferred mineral resources that are considered too speculative geologically to have economic considerations applied to them that would enable them to be categorized as mineral reserves. The study is preliminary in nature and there is no assurance the mining, metal production or cash flow scenarios outlined in this report would ever be realized. Mineral resources are not mineral reserves and do not have demonstrated economic viability.

Forward looking statements

Certain statements in this news release are forward-looking statements, which reflect the expectations of management regarding the Turnagain Project. Forward-looking statements consist of statements that are not purely historical, including any statements regarding beliefs, plans, expectations or intentions regarding the future. Such statements include, but are not limited to, statements with respect to the future financial or operating performance of the Company and its mineral projects, the estimation of mineral resources and mineral prices, steps to be taken towards commercialization of the resource, the timing and amount of estimated future production and capital, operating and exploration expenditures, and the expectation that the risk level is lower than some other mining projects; that our project is similar in many ways and in some ways favourably comparable to other nickel projects; that battery companies will use much more nickel in future; that a price premium could accrue to a nickel mine that was genuinely carbon neutral; and that we can produce nickel with low net carbon emissions. Such statements are subject to risks and uncertainties that may cause actual results, performance or developments to differ materially from those contained in the statements. No assurance can be given that any of the events anticipated by the forward-looking statements will occur or, if they do occur, what benefits the Company will obtain from them. These forward-looking statements reflect management's current views and are based on certain expectations, estimates and assumptions which may prove to be incorrect, including the statements relating to future exploration and development of the Project and mineral resource and mineral reserve estimations relating to the Project. A number of risks and uncertainties could cause our actual results to differ materially from those expressed or implied by the forward-looking statements, including: (1) the mineral resource estimates relating to the Project could prove to be inaccurate for any reason whatsoever, (2) Giga is unable to finance the Project, (3) prices for nickel and cobalt or project costs could differ substantially and batteries may not in future depend on nickel (4) inferred and indicated resources may not materialize, (5) permits, environmental opposition, government regulation, cost overruns or any of many other factors may prevent the Company from commercializing the Turnagain Project, (6) additional but currently unforeseen work may be required to advance to the pre-feasibility stage, (7) risk may be higher than expected for a number of reasons, some foreseeable and others unforeseeable such as indigenous land claims, natural disaster, and many other possibilities; (8) despite our expectations that we are comparable to other nickel projects, on closer examination and upon project start-up we may find that our expected comparisons were not valid; and (9) even if the Project goes into production, there is no assurance that operations will be profitable or that we can reduce carbon emissions compared to other producers. These forward-looking statements are made as of the date of this news release and, except as required by applicable securities laws, the Company assumes no obligation to update these forward-looking statements, or to update the reasons why actual results differed from those projected in the forward-looking statements. Additional information about these and other assumptions, risks and uncertainties are set out in the "Risks and Uncertainties" section in the Company's most recent MD&A filed with Canadian security regulators.

On behalf of the Board of Directors,

“Martin Vydra”

MARTIN VYDRA, President

GIGA METALS CORPORATION

Tel - 604 681 2300

Neither TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.